Which is a better investment plan Systematic Withdrawal Plan(SWP) or Annuity?

Updated on 22-02-2020

Ah! Who will not enjoy their retirement, free from routine work, working for passion rather than the money?

Almost all the retiring person, particularly employee, start calculating their inflow of fund that they will get on their retirement and start preparing their wish list for expending that money. upgrading of house, going on foreign trip, upgrading Car, making investment in some scheme that was referred by his friend etc.

As it is tough to control emotion while sudden flow of huge money. People starts making mistakes by forgetting or miscalculating their regular livelihood expenses, inflation or any compulsory liability like daughter marriage etc. This result to throw them in financial crisis problem on his growing age.

The common confusion arrives to the retiring person of parking their retirement corpus to generate their livelihood expenses. Most of the person get misled by market force and invest their corpus either in low yielding schemes or very risky instruments like equity, low rated NBFC, pongee scheme, etc. and in both cases result are same, inviting crisis phases on older ages.

If you are planning monthly income for your retirement in coming years by investing money in some financial product, a Systematic Withdrawal Plan (SWP) of a mutual fund may be one of the best options for you instead of annuity expected you draw a complete risk appetite and allocation strategy in proper manner. You may find many financial planners on google search, GIIS Financial a financial planning firm among them having good reputation and client service tools.

What is SWP?

A Systematic Withdrawal Plan allows you systematic redemption of your invested money. This plan allows investors to withdraw their accumulated corpus over a period of time instead of evacuating all the money at once. This can provide you a fixed income every month that will come directly to your bank account.

Whereas Annuity is a contract which provides payouts to the subscriber of a scheme such as a pension plan. Where in lump sum payment is made by an individual to obtain certain amounts immediately or at some point of future.

“SWP is most suitable for retired people who can stay invested and take out only the amount that is needed at any point in time. Though SWP can be done from any fund that allows this plan, it is best to keep this money in debt fund and withdraw at a regular period.

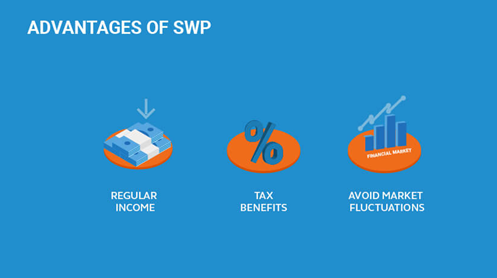

Tax Advantage

SWP is an option worth exploring for those who want a regular income.

If you invest in an annuity scheme for regular income, the interest income or annuity payment will be taxed at the marginal income tax rate.

However, in case of an SWP, your income is on account of redemption of units. Hence, capital gains tax will apply, which can be favorable if you have held the units for the long term.

Systematic Withdrawal Plan mutual fund innovation to compete with annuities. Annuity and SWP are based on the same principle of fixed withdrawal.

- An annuity is guaranteed based on the plan that you have chosen but is taxable. Once you buy an annuity you don’t have any control over that money.

- In SWP there is no guarantee but you have the option to increase or decrease withdrawal amount.

- Annuity is not inflation adjusted whereas with SWP you can build that plan.

Let us understand it through an example

Suppose you invested Rs 15 lakhs at the time of retirement in a balanced mutual fund and then you run an SWP of Rs 15000 per month. Assuming the fund gives a return of 10% per annum, your funds will last you for 211 months (Approximately 17.5 years). If your annual withdrawal is less than the expected annual rate of return, or your fund is giving more returns year on year then the SWP can run perpetual, that is, you can get monthly income forever by doing one-time investment.

SWP allows the investor to stay invested and save and take out only required amount.

Hence SWP is a better investment plan than the Annuity.

Not sure which mutual funds to Buy?

Speak to GIIS financial Professionals and get investment recommendations.

You can use GIIS Financial tools or Our Android App for Investment, tracking and Asset allocation planning.

*Mutual Fund Investments are subject to market risk, read all scheme related documents carefully.

Share On

0

Comment